If you have ever watched your credit score drop even though you paid your bill on time every single month, credit utilization is almost certainly the explanation. It is the second most heavily weighted factor in the most widely used credit scoring models, sitting just behind payment history in importance, yet most people have never encountered the term until they notice a score change they cannot explain. Understanding how utilization works changes how you manage your credit cards and gives you a direct lever for improving your score that produces real results faster than almost any other approach available.

How Credit Utilization Is Calculated

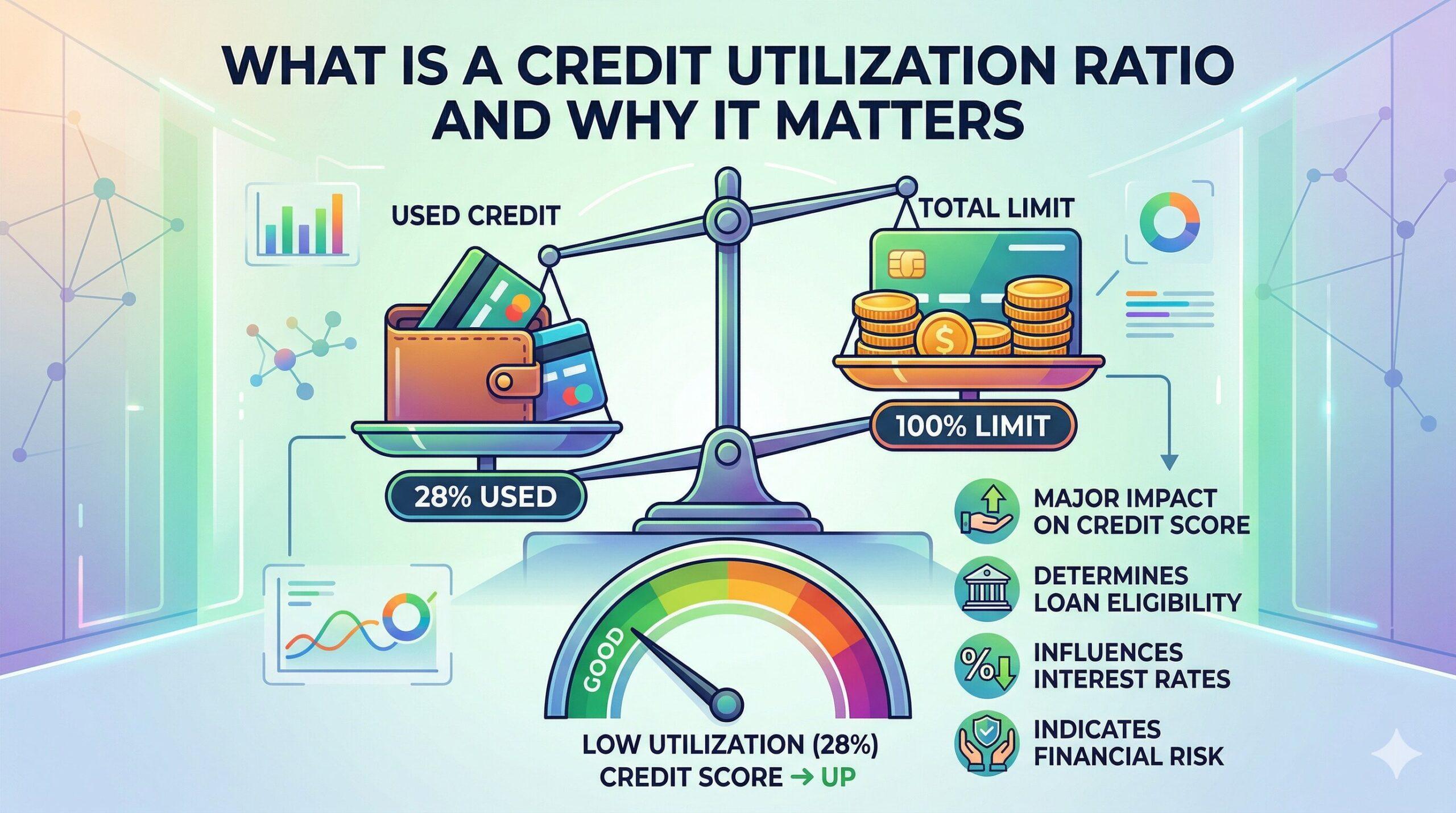

Your credit utilization ratio is the percentage of your total available revolving credit that you are currently using. If you have a credit card with a five thousand dollar limit and you are carrying a balance of two thousand five hundred dollars, your utilization on that card is 50 percent. Most scoring models calculate utilization in two ways: per-card utilization on each individual revolving account and overall utilization across all revolving accounts combined. Both figures are considered, and a high ratio on even one card can drag down your overall score even if your total utilization across all accounts looks moderate. The widely cited guidance is to keep utilization below 30 percent, though people with the strongest scores typically stay below 10 percent, and any meaningful reduction in utilization generally produces a score improvement at the next reporting cycle.

Here is where the mechanics trip people up consistently. Paying your statement balance in full every month is excellent for avoiding interest charges, but it does not necessarily mean the credit bureaus see a low balance on your account. Most card issuers report your balance to the bureaus on your statement closing date, which is typically before your payment due date. If your statement closes on the 15th showing a balance of three thousand dollars and you pay it in full on the 20th, the bureaus record that three thousand dollar balance for the full reporting period. The fix is to make a payment before your statement closing date so that the balance your issuer reports is lower than what you actually spent during the month.

It is also worth understanding that utilization applies specifically to revolving credit accounts, meaning credit cards and personal lines of credit. Installment loans like auto loans, student loans, personal loans, and mortgages do not factor into your utilization ratio even though they appear on your credit report. Managing the reported balance on your credit cards is the specific behavior that drives this component of your score, and confusing utilization management with general debt reduction leads to effort directed at the wrong accounts.

Common Mistakes That Hurt Your Utilization

One of the most common and counterintuitive utilization mistakes is closing a credit card you are no longer actively using. It feels like responsible financial simplification, but closing an account reduces your total available credit immediately. If you have fifteen thousand dollars in available credit across three cards and you close one with a five thousand dollar limit, your available credit drops to ten thousand. A two thousand dollar balance that represented roughly 13 percent utilization now represents 20 percent. The score impact can be both immediate and meaningful, which is why keeping older accounts open with occasional small purchases to prevent issuer-initiated closure is often the better financial decision.

There is also a timing adjustment worth building into your monthly routine. Most credit cards let you check your statement closing date in the account settings. Once you know that date, scheduling a larger payment a few days before it arrives each month rather than waiting for the due date keeps your reported utilization consistently lower without changing your actual spending. Credit utilization resets monthly based on what your issuer reports, which makes it one of the most actionable factors available for someone working to improve their score within a defined timeframe.One more thing worth understanding about utilization is how it interacts with credit limit increases. If your card issuer offers you a higher credit limit, accepting it lowers your utilization percentage on that card without requiring you to change your spending at all. A balance of two thousand dollars on a card with a four thousand dollar limit represents 50 percent utilization. The same two thousand dollar balance on a card with an eight thousand dollar limit represents only 25 percent. Requesting a credit limit increase when your account is in good standing and your income has increased is a legitimate and often underused strategy for improving your utilization ratio.

Leave a Reply