Building a strong credit profile often feels like trying to open a door that requires a key you do not yet have in your possession. For many young adults, recent immigrants, or individuals recovering from past financial mistakes, the traditional path to credit is blocked by a lack of history. This is where the concept of becoming an authorized user serves as a powerful and strategic bridge toward financial independence. When a primary cardholder adds you to their account, you essentially “piggyback” on their established habits and the age of that specific line of credit. It is a unique relationship where the credit card issuer reports the activity of the account under both the name of the owner and the name of the authorized person. While this sounds like a simple shortcut, the underlying mechanics of how this status impacts your FICO and VantageScore numbers are actually quite complex and require careful management.

An authorized user is someone who has permission to use a credit card account but is not legally responsible for paying the bill. This distinction is critical because it separates you from the “joint account holder” status where both parties are on the hook for the debt. Despite this lack of legal liability, the positive data from that account flows onto your credit report as if the history were partially your own. If the primary user has managed the card perfectly for ten years, you may suddenly see a decade of “perfect” payment history appear on your report overnight. This can result in a dramatic increase in your score, sometimes by dozens of points, because it instantly addresses the “length of credit history” and “payment history” categories that make up the majority of your total score calculation. However, you must ensure the card issuer actually reports authorized user data to the three major bureaus—Equifax, Experian, and TransUnion—before you agree to the arrangement.

The Mathematical Impact of Utilization and Account Age

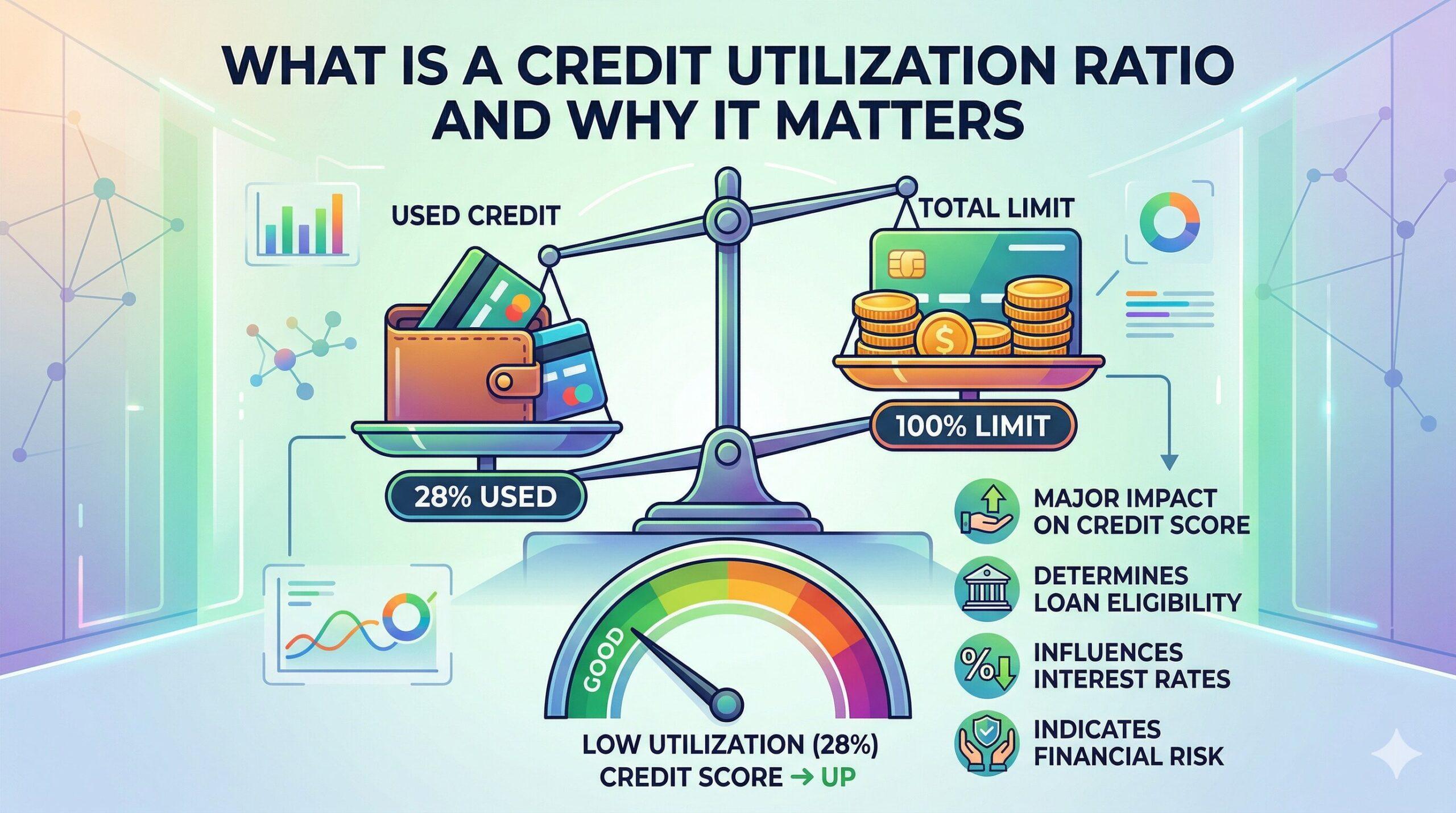

The most immediate benefit of becoming an authorized user is the expansion of your total available credit limit, which directly improves your credit utilization ratio. Credit utilization is the percentage of your available credit that you are currently using, and keeping this number below thirty percent is vital for a high score. When you are added to an account with a $10,000 limit and a zero balance, your total available credit increases by that full amount without adding any new debt. If you currently have a small $500 starter card that is nearly maxed out, your utilization will drop from nearly one hundred percent to less than five percent instantly. This shift signals to lenders that you are not desperate for credit, making you appear much more attractive as a borrower for future loans or your own independent credit cards.

Account age is another heavy hitter in the credit score formula, and authorized user status allows you to “inherit” time. The “Average Age of Accounts” metric is often a weak point for people who have only recently started their financial journey. By being added to an older account—perhaps one your parents or a spouse has held since the early 2000s—you significantly pull up the average age of all the accounts listed in your name. This long-term data provides a sense of stability that a brand-new account simply cannot offer. It tells the scoring algorithms that you have been associated with a well-managed financial tool for a long duration, which helps mitigate the risk profile associated with “thin” credit files. You should always ask the primary cardholder how long they have owned the account and if they have ever missed a payment before you let them add your name.

Navigating the Risks of Negative Reporting and Mismanagement

While the benefits of authorized user status are substantial, the relationship is a two-way street that carries a significant amount of risk if the primary cardholder is not disciplined. Because the account data is shared, any negative actions taken by the primary owner will show up on your credit report with the same weight as the positive ones. If the person who added you suddenly misses a payment by thirty days or more, your credit score will likely plummet as a result of their mistake. Similarly, if they decide to max out the card to pay for a large emergency, your utilization ratio will spike across the board. In some cases, the “damage” from a poorly managed authorized account can be worse than having no credit history at all, as it introduces fresh derogatory marks that stay on your record for years.

The secondary risk involves the social and personal dynamics between you and the primary account holder. Even though you are not legally obligated to pay the bill, spending money on the card without a clear agreement on reimbursement can destroy trust and lead to the primary user removing you from the account. When you are removed as an authorized user, the entire history of that account—including the age and the limit—is usually deleted from your credit report entirely. This means the “score boost” you enjoyed will disappear as quickly as it arrived, potentially leaving you in a worse position if you have not used the temporary boost to open your own independent lines of credit. It is best to treat the authorized user card as a “read-only” tool; you do not even need to have the physical card in your wallet to benefit from the credit reporting aspect of the arrangement.

Strategic Steps for Long Term Credit Independence

The ultimate goal of using authorized user status should be to build enough of a foundation to qualify for your own credit products. It is a temporary training wheel, not a permanent solution for financial health. While you are benefiting from someone else’s good habits, you should use that time to apply for a secured credit card or a low-limit retail card in your own name. Once you have your own accounts, you begin to build a “primary” history that cannot be taken away if the authorized user relationship ends. Lenders who look manually at your credit report, such as mortgage underwriters, often distinguish between authorized user accounts and your own accounts. They want to see that you can manage debt when you are the one legally responsible for the monthly payments and the interest charges.

To maximize this strategy, you must communicate clearly with the primary cardholder about their future plans for the account. Ask them to set up automatic payments so there is zero chance of a late payment ever touching the record. You might also suggest that they set a “spending alert” on the card to ensure the balance never exceeds a certain percentage of the limit. If you notice the primary user is starting to struggle financially, you have the right to contact the credit card issuer and ask to be removed from the account yourself. This “self-removal” is a vital safety valve that allows you to protect your score from a sinking ship. By combining the inherited history of an authorized user status with the responsible management of your own new accounts, you can build a robust, high-scoring credit profile that will serve you for the rest of your life.

Leave a Reply