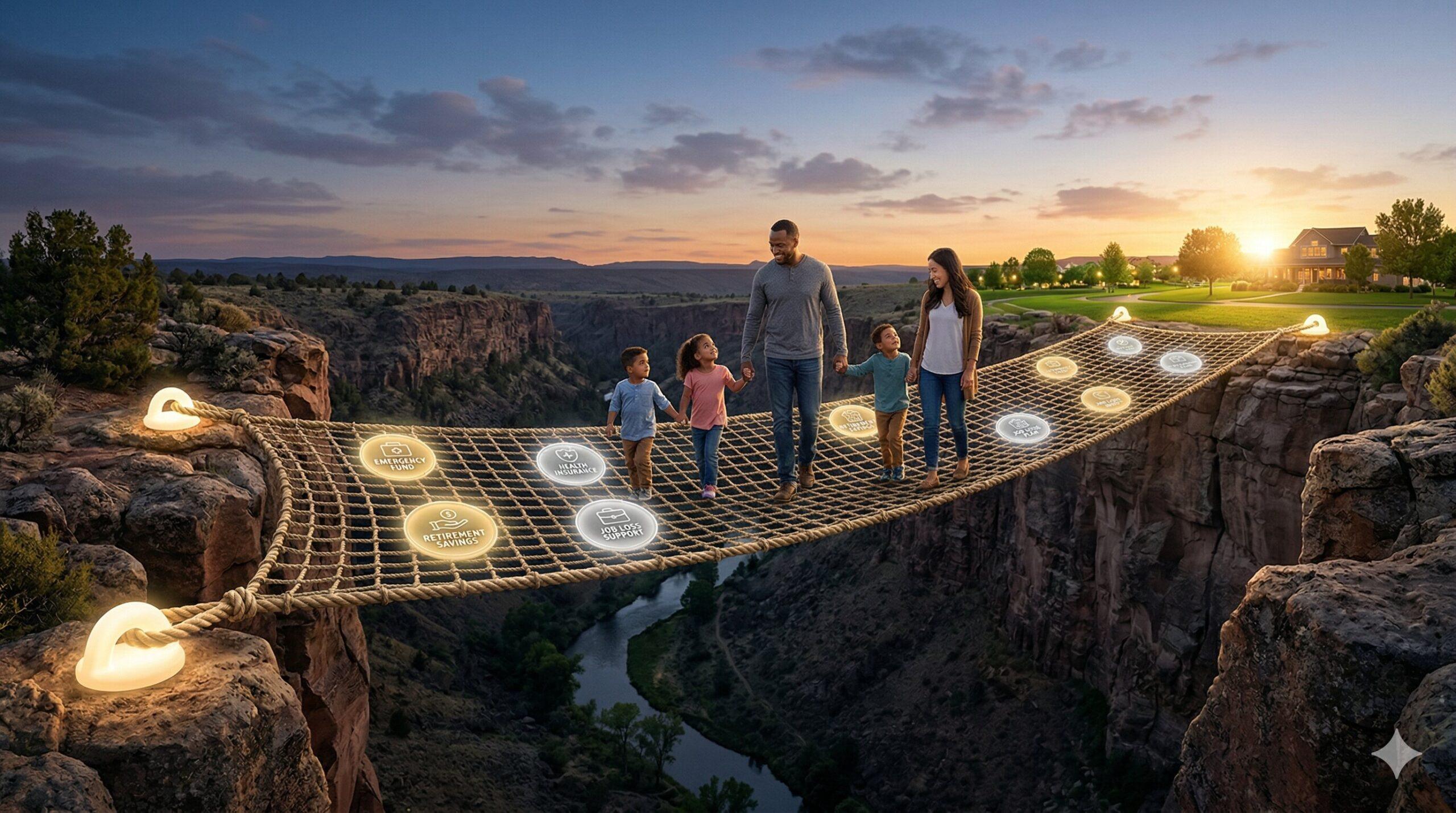

The phrase financial safety net gets used so often that it has started to lose its meaning. People hear it and think of emergency funds, picturing a savings account with three to six months of expenses sitting in it. That version of the safety net is real and worth building, but a complete financial safety net is actually a layered system of resources that includes savings, government programs, community support, and insurance all working together to absorb shocks of different sizes and durations. No single piece of that system protects you adequately on its own, and most people have larger gaps than they realize until something goes wrong.

Why One Layer Is Never Enough

Think about what actually happens when something goes wrong financially. A job loss does not create just one problem. It creates a cascade. The income stops. The health insurance tied to that job disappears at the same time. Bills that were manageable suddenly are not. If you have savings, you draw them down faster than expected because multiple costs are hitting simultaneously. A savings account absorbs some of that pressure, but unemployment insurance absorbs another portion. Medicaid or marketplace coverage handles the health piece. SNAP handles the grocery piece. Each layer of the safety net is designed to catch a different part of the fall, and together they prevent a manageable setback from turning into a genuine financial spiral.

Building a complete safety net means understanding what each layer is designed to cover before you actually need any of it. Personal savings are your first line of defense, most useful for disruptions that last a few weeks or a few months. Government benefit programs are your second line, designed for disruptions that stretch longer or hit harder than savings alone can handle. Community resources including food banks, local assistance funds, and nonprofit organizations are your third line, filling gaps where government programs have eligibility thresholds or funding limitations. Insurance in all its forms is your fourth line, protecting against catastrophic events that would otherwise wipe out all three other layers at once.

The reason most people underestimate the importance of building all four layers is that each one feels optional until it is the only thing standing between you and a serious crisis. Health insurance feels unnecessary until you face a hospitalization that costs tens of thousands of dollars. An emergency fund feels optional until an urgent repair drains a bank account that cannot quickly recover. The cumulative cost of not having these layers when you need them is always higher than the effort required to build them while you have the stability to do so deliberately.

How to Find the Gaps in Your Safety Net

Most people have something resembling one or two layers but not all four working together. A household might have decent savings but no awareness of what government programs they currently qualify for. Another might have Medicaid and SNAP enrolled but no emergency savings and no disability insurance to cover an extended illness. Both situations carry real vulnerability, just pointing in different directions.

One practical way to start building when savings feel out of reach right now is to focus on the enrollment side first. Signing up for every government program your household currently qualifies for, even programs you do not immediately need, keeps those resources available and active when circumstances change unexpectedly. Knowing your SNAP eligibility before a job loss means one fewer process to navigate during the most stressful period. The safety net works best when its components are already in place before you need to lean on any of them, and enrollment costs nothing except the time it takes to complete the application.

One resource that spans multiple layers of the safety net is your local community action agency, which typically administers LIHEAP and other government programs while also running emergency assistance funds, food pantries, and financial coaching programs all in the same organization. A single intake appointment at a community action agency can connect you to multiple layers of support simultaneously rather than requiring separate applications to each individual program. Finding your local agency through the Community Action Partnership website or through 211 is the fastest way to access this kind of coordinated support.

Leave a Reply