When people talk about financial assistance, the words grant, loan, and subsidy get used almost interchangeably, and that creates real confusion when someone is trying to understand what kind of help they are actually receiving. These three things work differently, carry different obligations, and affect your financial situation in very different ways. Mixing them up can mean accepting debt you did not intend to take on, missing a benefit you are fully entitled to, or making financial decisions based on a fundamental misunderstanding of what a program actually provides. Getting clear on the distinctions before you apply is worth the few minutes it takes.

Grants and Loans Are Not the Same Thing

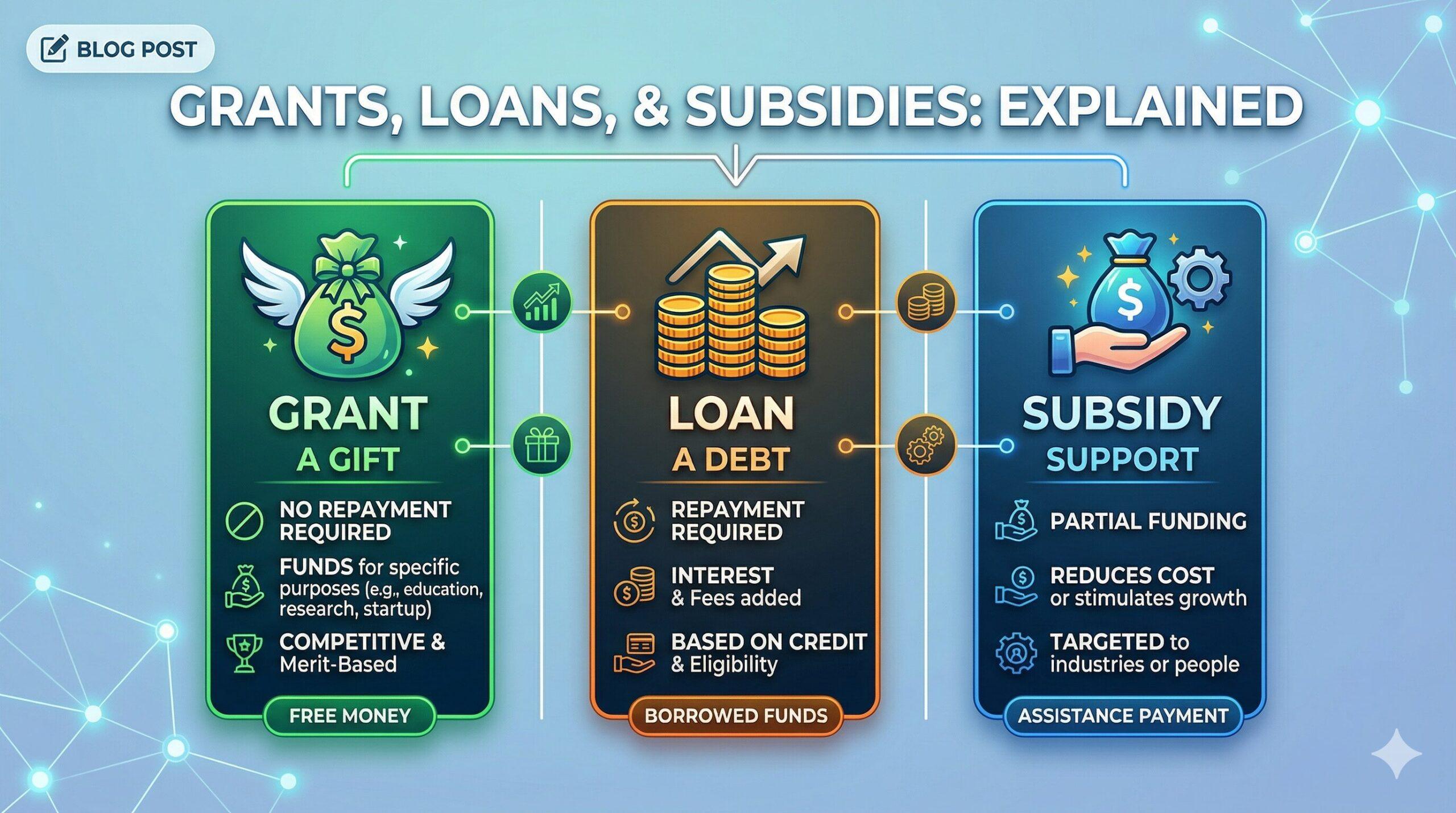

A grant is money you receive that you do not have to repay. It comes from a government agency, a private foundation, or a nonprofit organization, and it is awarded to support a stated purpose or address a documented need. Federal Pell Grants for education, LIHEAP energy assistance payments, HOME housing rehabilitation funds, and small business grants from state economic development agencies are all genuine grants. The essential feature is the absence of a repayment obligation, provided you use the funds for their intended purpose and continue meeting program requirements. Grants may have eligibility criteria, reporting requirements, and conditions around how the money is spent, but they do not create debt and they do not appear on your credit report.

A loan is money you borrow with a contractual obligation to repay it, typically with interest, over a defined period. Student loans, personal loans, SBA business loans, and even low-interest emergency loans from state assistance programs are all loans regardless of how they are described in program materials. The fact that a loan has a favorable interest rate, a deferred payment period, or a government origin does not change its fundamental nature as debt. Loans affect your credit profile, carry repayment schedules, and have legal consequences if you default. Some loans contain forgiveness provisions, such as Public Service Loan Forgiveness for federal student loans, but forgiveness is conditional and must be explicitly confirmed in writing before you can rely on it.

Understanding this distinction is especially important when reviewing program materials that use softened language. Terms like financial support, assistance payment, emergency award, and relief benefit can describe either a grant or a loan depending on the specific program. If program materials do not clearly state that no repayment is required, ask directly and get that answer confirmed in writing before you accept anything. Programs with nothing to hide answer this question immediately.

What a Subsidy Actually Means for You

A subsidy is a financial benefit that reduces what you pay for a product or service rather than giving you money directly. Premium tax credits that lower your monthly health insurance payment on the marketplace are a subsidy. The Affordable Connectivity Program discount applied to your internet bill is a subsidy. Section 8 housing choice vouchers are a subsidy. In each case you are not receiving cash in hand. The cost of something you are already purchasing or using is being reduced on your behalf. Subsidies generally do not need to be repaid, but they are contingent on continued eligibility. If your income rises above the qualifying threshold, the subsidy amount decreases or ends at your next eligibility review.

There is one important nuance worth understanding about advance payment subsidies. Marketplace premium tax credits are paid in advance before your actual annual income is confirmed, and the amount is reconciled on your federal tax return at year end. If your actual income turns out to be higher than you estimated when you enrolled, you may need to repay a portion of the advance credit when you file. This is not a penalty but the reconciliation of what was paid on your behalf against what you were actually entitled to receive.One situation where all three types of assistance can interact at the same time is health insurance. The premium tax credit is a subsidy. A health savings account funded with pre-tax dollars is a tax benefit. A nonprofit grant to cover a medical bill is a grant. Knowing which type you are dealing with at any given moment lets you use each one correctly and helps you avoid the kind of retroactive surprise that tends to appear at tax filing time when multiple types of assistance were received during the same calendar year. The practical takeaway is simple: know exactly what you are accepting before you accept it.

Leave a Reply