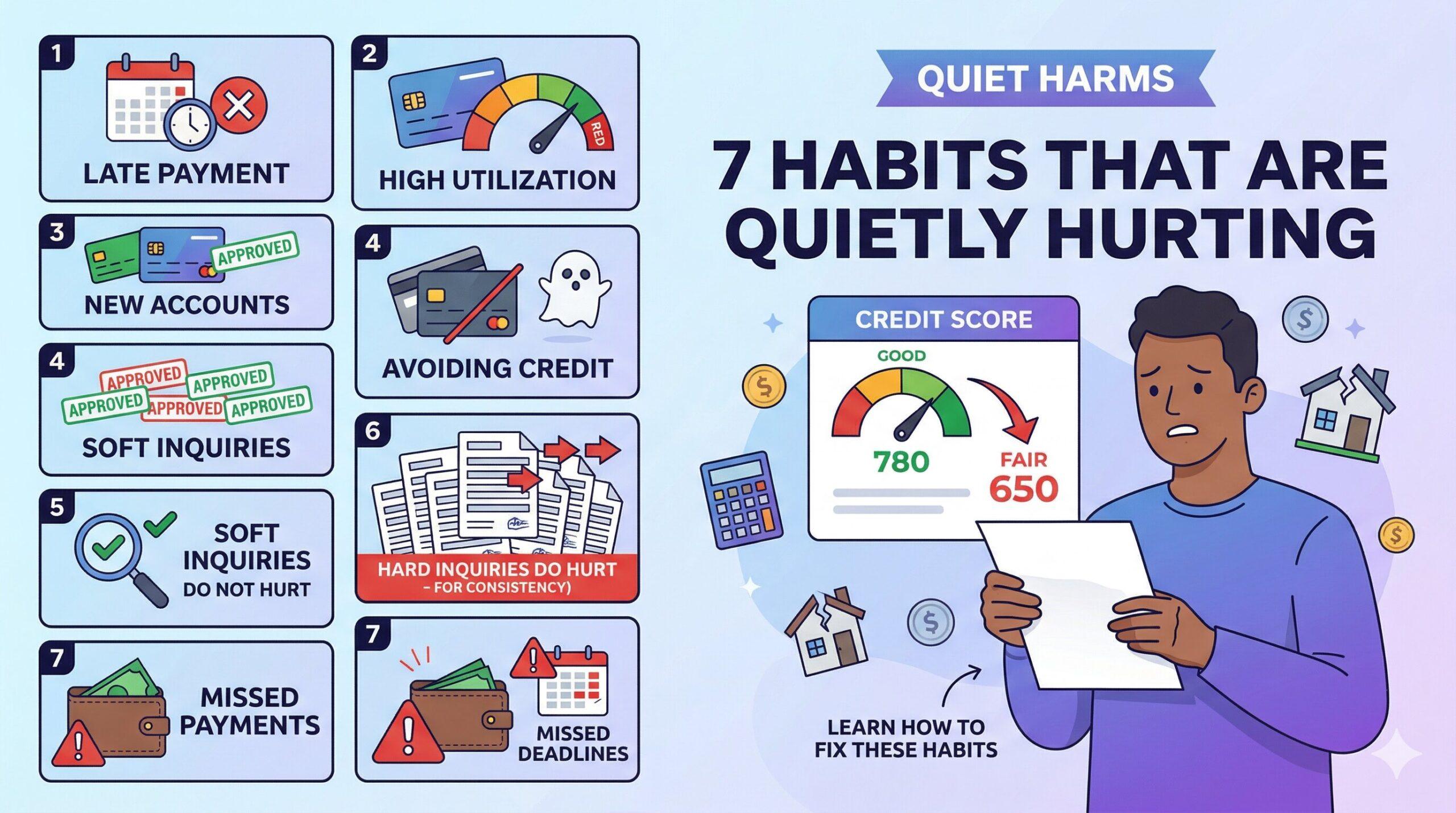

Some credit score damage is obvious. A missed payment, a collection account, or a bankruptcy all produce immediate and visible consequences that most people recognize as harmful. But a significant portion of credit score damage comes from habits that feel completely routine and sensible, behaviors that people engage in every month without ever connecting them to the gradual decline they eventually notice in their scores. These seven habits are common, quiet, and consistently costly over time. Recognizing them is the first step toward stopping the damage before it compounds further and becomes harder to reverse.

Habits Tied to How You Use Credit

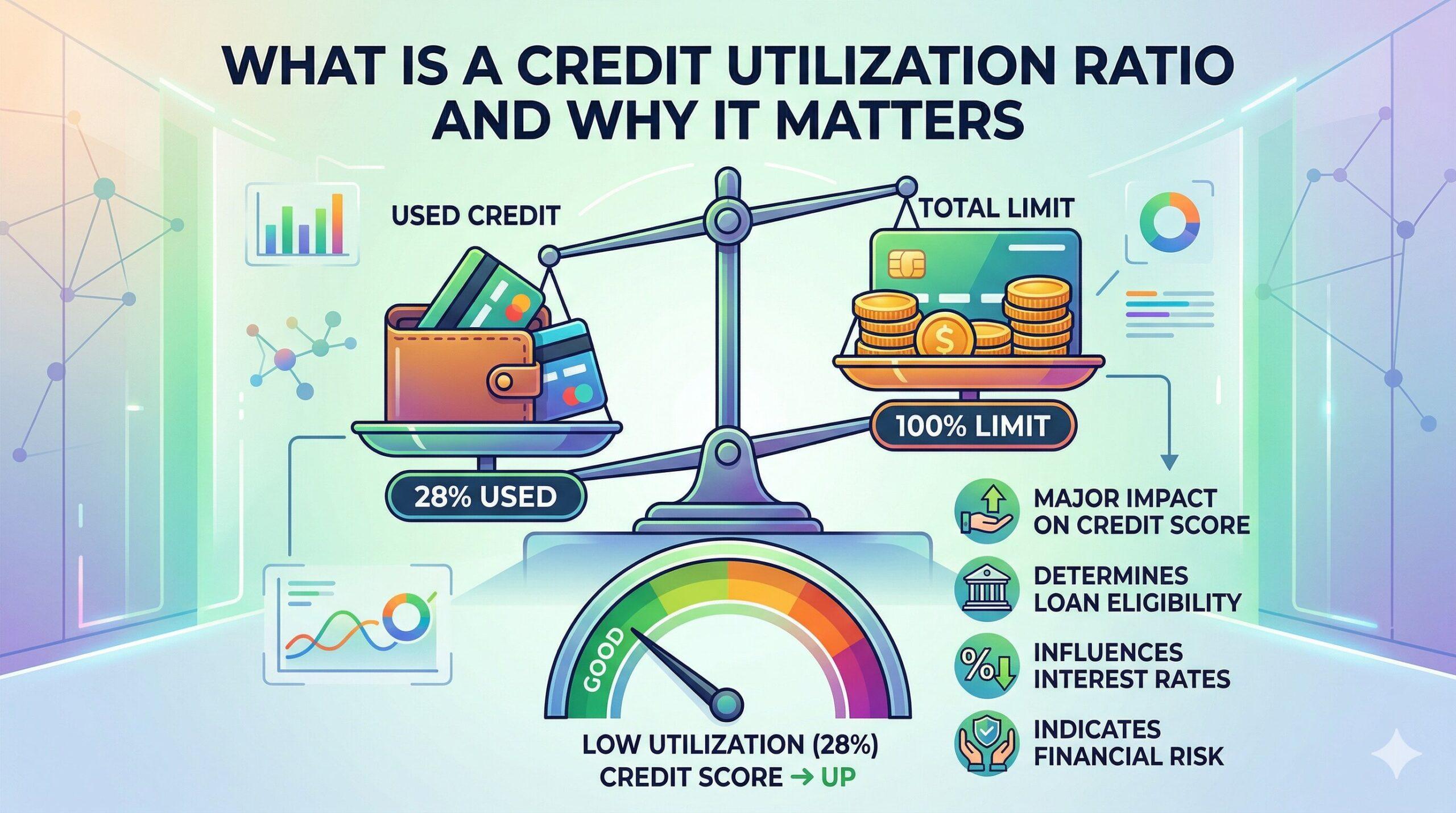

Carrying a high balance relative to your credit limit is the most widespread habit on this list. Even when you are paying the minimum on time without fail, a balance that regularly sits at 40, 50, or 60 percent of your available limit is generating a high utilization ratio that the credit bureaus record at every statement closing cycle. The score impact accumulates with each reporting period, and paying only the minimum due never fully resolves the underlying utilization problem. The only effective fix is paying the balance down meaningfully, ideally to below 30 percent of your limit before the statement closing date arrives each month.

Applying for multiple new credit products within a short period triggers a cluster of hard inquiries on your credit report. Each individual inquiry causes a small temporary dip, typically two to five points. The larger problem is that several inquiries appearing close together signal to scoring models that you may be experiencing financial stress and seeking new credit aggressively. Spacing out applications by at least six months between new credit products eliminates this pattern entirely and prevents the cumulative score impact that comes from clustered applications.

Closing credit card accounts you are not actively using is one of the most misunderstood habits on this list. It feels like responsible financial simplification. It often hurts your score by reducing your total available credit and potentially shortening your average account age. Keeping accounts open with occasional small purchases to prevent issuer-initiated closure is typically the better approach. Co-signing a loan for someone else places that loan on your credit report with the same weight as if you had taken it out yourself, meaning every missed payment by the primary borrower also appears as a missed payment on your file.

Habits That Seem Harmless Until They Are Not

Ignoring your credit reports entirely allows errors to sit uncorrected for years without your knowledge. A medical debt incorrectly attributed to your account, a payment marked late that you can document was made on time, or a fraudulent account opened in your name can drag down your score for years if you never check the underlying report to find and dispute it. Errors on credit reports are more common than most people expect, and the dispute process through each bureau’s online portal is straightforward once you know the error exists.

Paying utility, phone, and rent bills late without fully understanding the downstream credit risk is another habit that catches people off guard. These accounts are generally not reported to the bureaus under normal circumstances, meaning a late payment does not directly affect your score. What does affect your score significantly is when the account is referred to a collections agency after a sustained period of non-payment. A collection account can reduce a score by fifty to one hundred points or more and stays on your report for seven years from the original delinquency date. Treating these bills with the same urgency as credit accounts prevents the collections outcome from ever starting in the first place.Not having enough variety in your credit accounts is the quietest item on this list because it feels like a non-issue rather than an active harmful habit. Scoring models reward a mix of revolving credit like credit cards and installment credit like auto loans or personal loans. A credit profile that contains only one type has a natural ceiling below which the score tends to plateau regardless of how perfectly those existing accounts are managed. The common thread connecting all seven habits is that each one involves either a misunderstanding of how the scoring system works or a routine behavior that produces negative outcomes when applied consistently. None of them require dramatic changes to fix, and recognizing them is always the most important first step.

Leave a Reply