Improving your credit score may seem like a long‑term project, but with focus and discipline, meaningful progress can be made in just 90 days. Lenders use credit scores to evaluate your reliability, and even small improvements can open doors to better loan terms, lower interest rates, and increased financial opportunities. This guide explains step by step how to improve your credit score in three months, highlighting practical strategies and tools that deliver results.

Understand Your Credit Report

The first step in improving your credit score is understanding where you stand. Request a free copy of your credit report from major bureaus such as Equifax, Experian, or TransUnion. Review the report carefully to identify errors, late payments, or high balances. Understanding your report helps you pinpoint areas for improvement. Correcting mistakes alone can lead to immediate score increases.

Dispute Errors Promptly

Errors on credit reports are more common than many realize. Incorrect account balances, duplicate entries, or misreported late payments can drag down your score. File disputes with the credit bureau to correct inaccuracies. Provide documentation such as payment receipts or bank statements. Disputing errors promptly ensures your score reflects your true financial behavior. Corrections often appear within weeks, making this an effective short‑term strategy.

Pay Bills on Time

Payment history is the most important factor in credit scoring. Late payments can significantly damage your score, while consistent on‑time payments improve it. Set reminders, use automatic payments, or create a calendar to track due dates. Paying bills on time for 90 days demonstrates reliability and builds positive history. Even small accounts such as utilities or phone bills contribute to your overall credit profile.

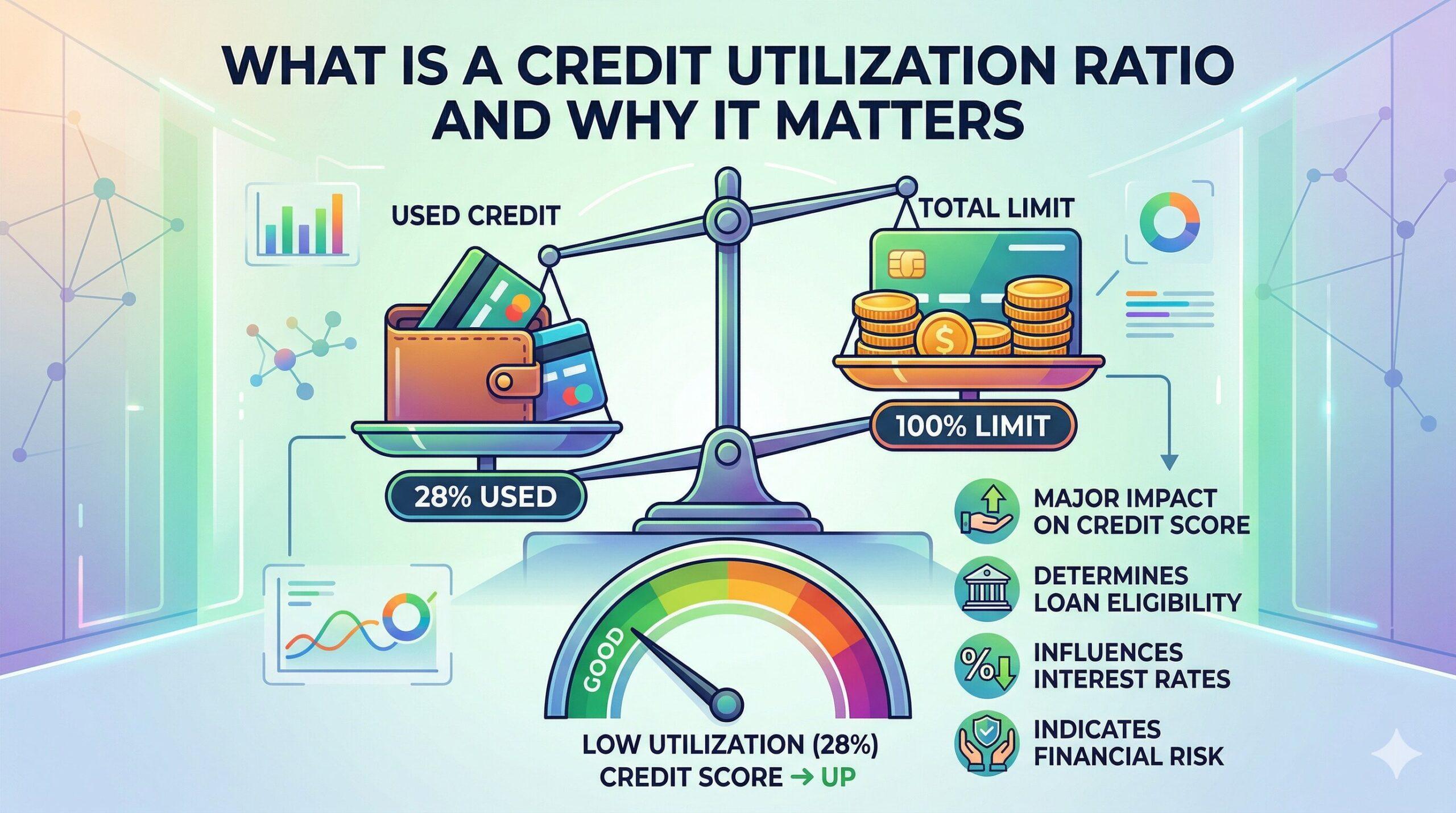

Reduce Credit Card Balances

High credit card balances increase your credit utilization ratio, which negatively impacts your score. Aim to reduce balances to below 30 percent of your credit limit, and ideally closer to 10 percent. Focus on paying down high‑interest cards first, while making minimum payments on others. Reducing balances quickly lowers utilization and improves your score within the 90‑day window.

Avoid New Debt

Taking on new debt during the 90‑day improvement period can undermine progress. New accounts create hard inquiries, which temporarily lower your score. Additional debt also increases utilization. Avoid applying for new loans or credit cards unless absolutely necessary. Focus on managing existing accounts responsibly. Avoiding new debt ensures your efforts remain effective.

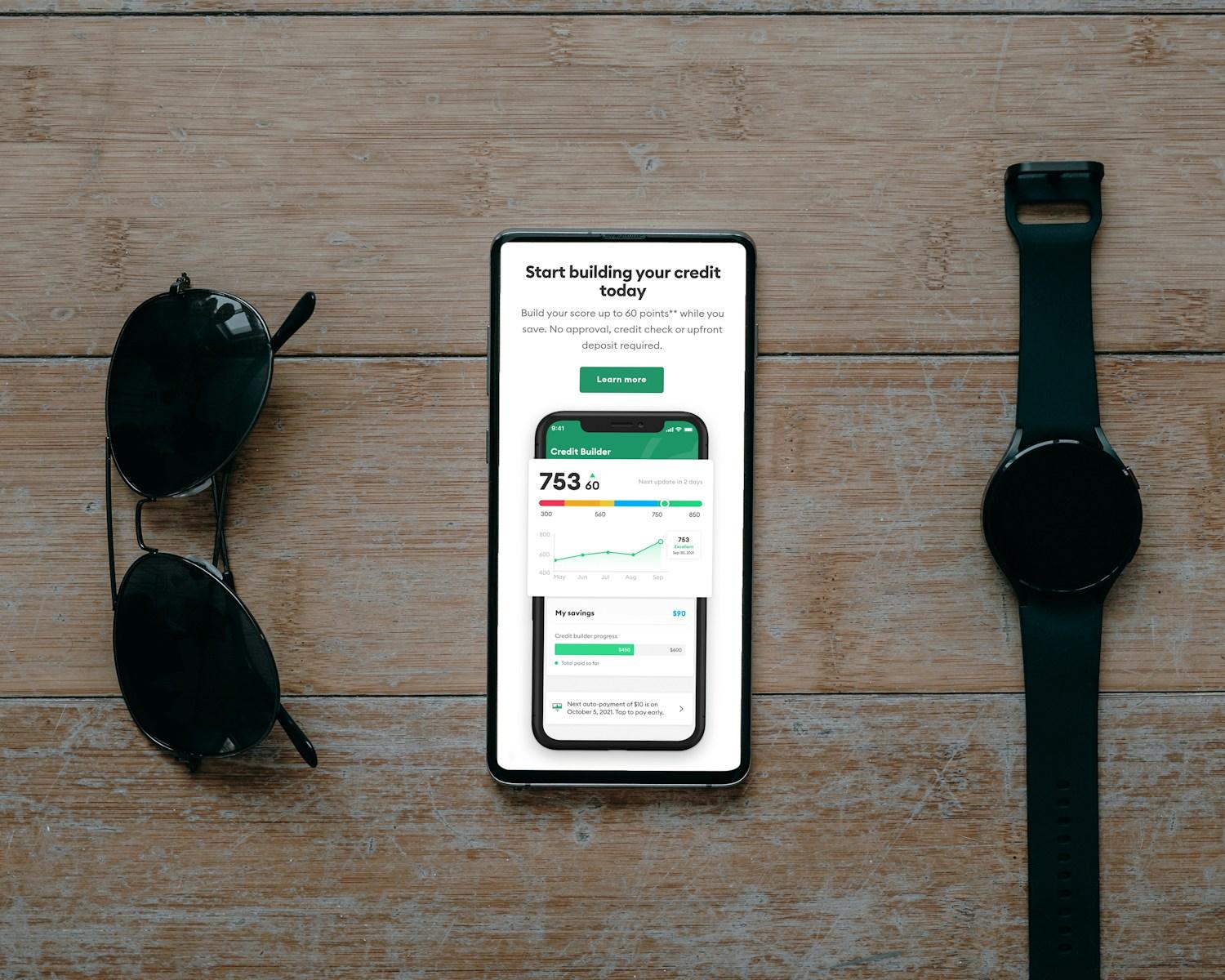

Use Secured Credit Cards

For individuals with limited or damaged credit, secured credit cards provide a powerful tool for improvement. These cards require a deposit that acts as collateral, making them accessible to more people. Using a secured card responsibly builds positive payment history and lowers utilization. One of the key secured card benefits is that activity is reported to credit bureaus, helping you establish or rebuild credit quickly. Within 90 days, consistent use of a secured card can show measurable improvement.

Keep Old Accounts Open

Length of credit history influences your score. Closing old accounts reduces average account age and may increase utilization. Keep older accounts open, even if you do not use them frequently. Maintaining long‑standing accounts demonstrates stability and strengthens your profile. Keeping accounts open ensures your score benefits from established history.

Diversify Credit Mix

Credit scoring models consider the variety of accounts you manage. A healthy mix of credit cards, installment loans, and retail accounts demonstrates financial responsibility. While you should avoid new debt during the 90‑day period, responsibly managing existing accounts contributes to improvement. Diversifying your credit mix over time strengthens your score further.

Monitor Progress Regularly

Monitoring your credit score during the 90‑day period helps you stay motivated and track progress. Many banks and credit card companies provide free score updates. Monitoring allows you to see the impact of actions such as paying down balances or disputing errors. Regular updates reinforce discipline and encourage continued effort.

Communicate with Creditors

If you struggle to make payments, communicate with creditors before accounts become delinquent. Many lenders offer hardship programs, payment extensions, or reduced interest rates. Communicating proactively prevents negative marks on your report. Creditors appreciate transparency and may provide solutions that protect your score. Communication demonstrates responsibility and strengthens relationships.

Avoid Closing New Accounts Too Soon

If you recently opened accounts, avoid closing them within the 90‑day period. Closing accounts reduces available credit and increases utilization. Keep new accounts open and manage them responsibly. Over time, these accounts contribute positively to your score. Avoiding premature closures ensures your efforts remain effective.

Use Budgeting Tools

Budgeting tools help you manage expenses and prioritize debt repayment. Apps and spreadsheets track spending, highlight unnecessary costs, and allocate funds toward debt reduction. Using budgeting tools ensures you remain disciplined during the 90‑day period. Effective budgeting supports timely payments and reduced balances, both of which improve your score.

Seek Professional Guidance

If you feel overwhelmed, consider seeking professional guidance. Nonprofit credit counseling agencies provide advice on managing debt and improving scores. Counselors help you create realistic budgets and repayment plans. Professional guidance ensures you make informed decisions and avoid risky shortcuts. Support from trusted organizations strengthens your financial resilience.

Plan for Long‑Term Stability

Improving your score in 90 days is achievable, but long‑term stability requires ongoing effort. Continue paying bills on time, keeping balances low, and monitoring reports regularly. Plan for future goals such as buying a home or financing education. Long‑term strategies ensure your score remains strong beyond the initial improvement period.

Improving your credit score in 90 days involves understanding your report, disputing errors, paying bills on time, and reducing balances. Avoiding new debt, using secured credit cards, and maintaining old accounts strengthen your profile. Monitoring progress, communicating with creditors, and using budgeting tools ensure success. Secured card benefits provide a powerful tool for individuals rebuilding credit, with activity reported to bureaus for quick improvement. With discipline, accountability, and long‑term planning, you can achieve meaningful progress in just three months and build a foundation for lasting financial stability.

Leave a Reply