Your credit score is influenced by several important factors, and credit utilization is consistently one of the most impactful. Many people focus entirely on making payments on time and ignore this number until something goes wrong with their score. That is a costly mistake that is easy to avoid once you understand how the ratio works. Keeping your utilization low is one of the fastest and most direct ways to improve your score without opening any new accounts or waiting years for old negatives to age off your report. Best of all, every improvement shows up in your score within a single billing cycle.

What Credit Utilization Ratio Means

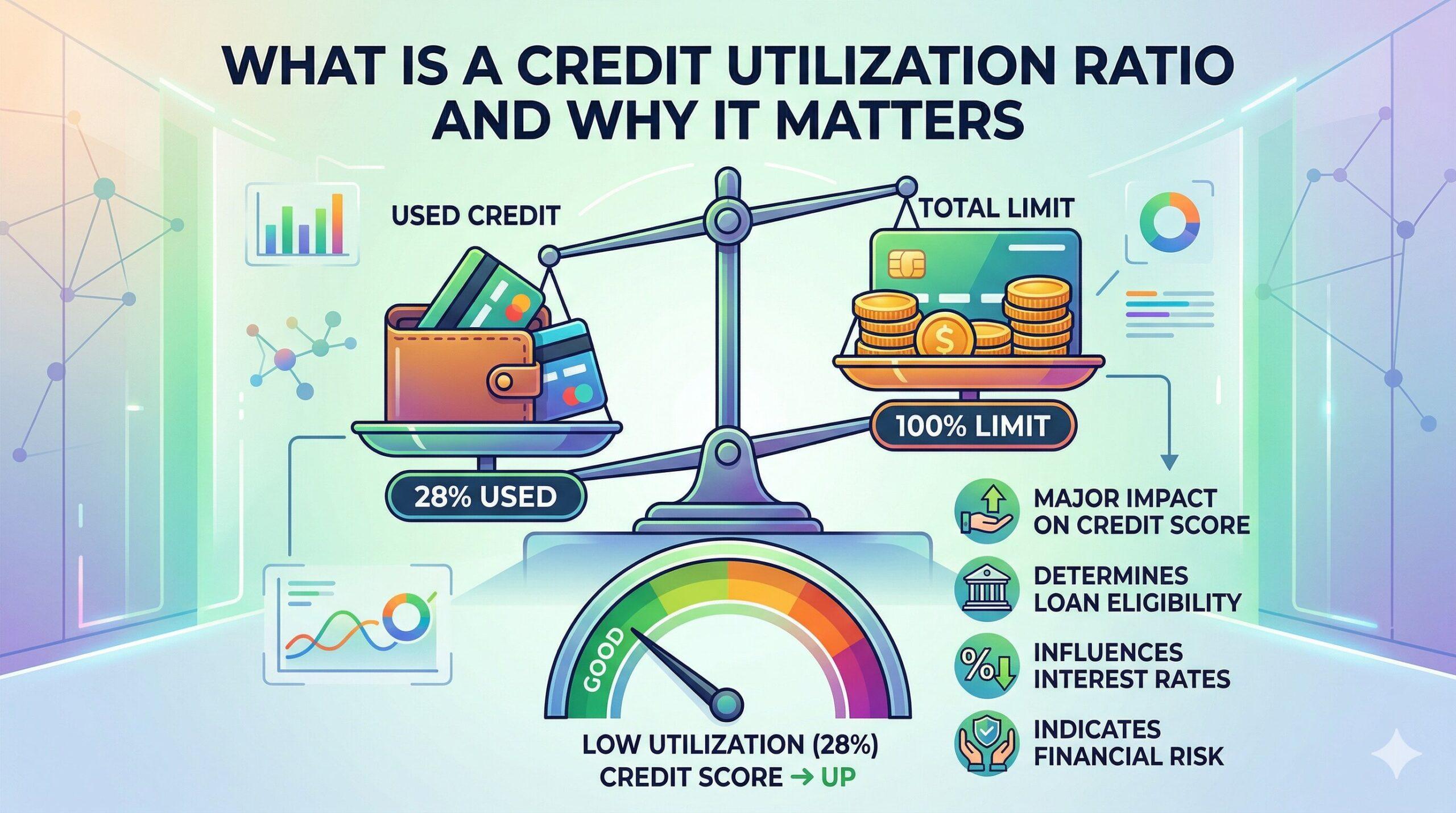

Your credit utilization ratio is the percentage of your total available revolving credit that you are currently using at any given time. Revolving credit includes credit cards and personal lines of credit but does not include installment loans like car loans or mortgages. The calculation is straightforward and takes only a moment to do. Divide your total credit card balances by your total credit card limits and multiply the result by 100.

For example, if you have two credit cards with a combined limit of $5,000 and you currently owe $1,500, your utilization ratio is 30%. Most credit scoring experts recommend keeping this number below 30% at all times. The strongest credit scores typically belong to people who maintain their ratio below 10% consistently. Paying your balances down is the most direct and reliable way to improve this number starting this month.

Why It Has Such a Big Impact on Your Score

Credit utilization accounts for roughly 30% of your FICO score calculation each month. That makes it the second most influential factor in your score after your payment history. A high utilization ratio signals to lenders that you may be financially overextended and a higher lending risk. Even if you pay your minimum on time every month, a ratio above 50% can drag your score down by a significant number of points.

The ratio is measured at a single point in time, usually when your monthly statement closes. That means even temporary high balances from large purchases can affect your score for that billing cycle. Paying down your balance before the statement closing date rather than waiting for the payment due date makes a measurable difference. Timing your payments strategically gives you better score results each month without spending any extra money overall.

How to Lower Your Credit Utilization Ratio

There are two fundamental ways to lower your ratio. You pay down your existing balances, or you increase the total amount of credit available to you. Both approaches work on their own, and combining them produces faster results than either one alone.

These are the most practical ways to lower your utilization ratio:

- Pay down your highest balance cards first to drop your overall ratio quickly

- Make a mid-cycle payment before your statement closes each month

- Ask your credit card issuer for a credit limit increase without increasing your spending

- Keep old credit card accounts open even if you rarely or never use them

- Spread purchases across multiple cards to avoid concentrating balances on one account

Opening a new card does increase your total available credit and lowers your ratio instantly. However, a new application triggers a hard inquiry that temporarily reduces your score by a small amount. Use this strategy sparingly and only when you plan to manage the new account with the same discipline as your existing cards.

What a Good Ratio Looks Like in Practice

A person with $10,000 in total credit limits should aim to carry no more than $1,000 in total balances at any point in the month. That keeps their ratio at 10%, which most scoring models reward with the highest possible score improvements. Staying below $3,000 on a $10,000 combined limit keeps the ratio at 30%, which is still considered acceptable by most lenders for loan and card approvals.

Building credit history and managing your utilization ratio work together as two sides of the same strategy. Having accounts open and keeping the balances low is the winning combination for a strong and stable credit profile over time.

Setting up an emergency savings buffer reduces the likelihood that you will need to charge unexpected expenses to your credit cards. When emergencies get paid from savings rather than credit, keeping your utilization low becomes much easier to maintain consistently.

Your ratio updates every single month based on your statement balance. Start paying down your balances today and check your score next month to see the improvement. Even a small reduction in your overall balance this month produces a measurable change in your score by the time your next statement closes. The math works in your favor every time you reduce what you owe relative to your available limit.

Leave a Reply