Financial stability often feels like a solid floor beneath your feet until small cracks begin to appear in your daily spending habits. Most people do not realize they are entering a credit crisis until a lender denies an application or a collection caller rings their phone. Understanding the warning signs of a looming financial disaster is the best way to prevent a total collapse of your credit score and your peace of mind. A credit crisis is rarely a sudden event; it is usually the result of several months or years of subtle shifts in how you manage your monthly obligations. By identifying these patterns early, you have the opportunity to pivot your strategy and seek professional assistance before your options become limited to bankruptcy or long-term debt settlement.

The first major red flag is the consistent use of credit cards to pay for basic living necessities like groceries, gas, and utility bills. While using a card for convenience or rewards is a common practice, it becomes a crisis signal when you do not have the cash in your bank account to cover those specific charges. If your paycheck is entirely committed to paying off last month’s expenses, leaving you with no choice but to charge this month’s food to a high-interest card, you are trapped in a dangerous cycle of “robbing Peter to pay Paul.” This behavior indicates that your cost of living has officially outpaced your actual income, and without a significant change, your debt will continue to compound until you reach your maximum limits.

Behavioral Shifts in Debt Management and Payment Patterns

A significant sign of an approaching crisis is when you start making only the minimum payments on all your revolving accounts. While paying the minimum keeps your account in good standing and prevents late fees, it does almost nothing to reduce the actual principal balance of what you owe. When your statements arrive and you see that your balance remains virtually unchanged despite your monthly contribution, your debt is officially stagnant. This often leads to a second sign: an increasing total debt load even when you feel like you are not making large purchases. Interest charges on a $5,000 balance at a twenty-four percent rate add over $100 to your bill every single month, which can quickly erase any small payments you manage to make.

Another behavioral warning is “credit card shuffling,” where you move debt from one card to another through balance transfers just to avoid a payment or a high interest rate. While a strategic balance transfer can be a helpful tool for someone with a plan, doing it repeatedly without actually paying down the debt is a sign of desperation. You may also find yourself “laddering” your bills—deciding which utility or credit card to skip this month so you can afford to pay a different one. If you are constantly calculating which late fee is the least expensive or which company takes the longest to send a shut-off notice, you are already in the middle of a credit crisis. This level of financial stress often leads to a “head in the sand” approach where you stop opening your mail or checking your bank balances because the reality of the numbers is too overwhelming to face.

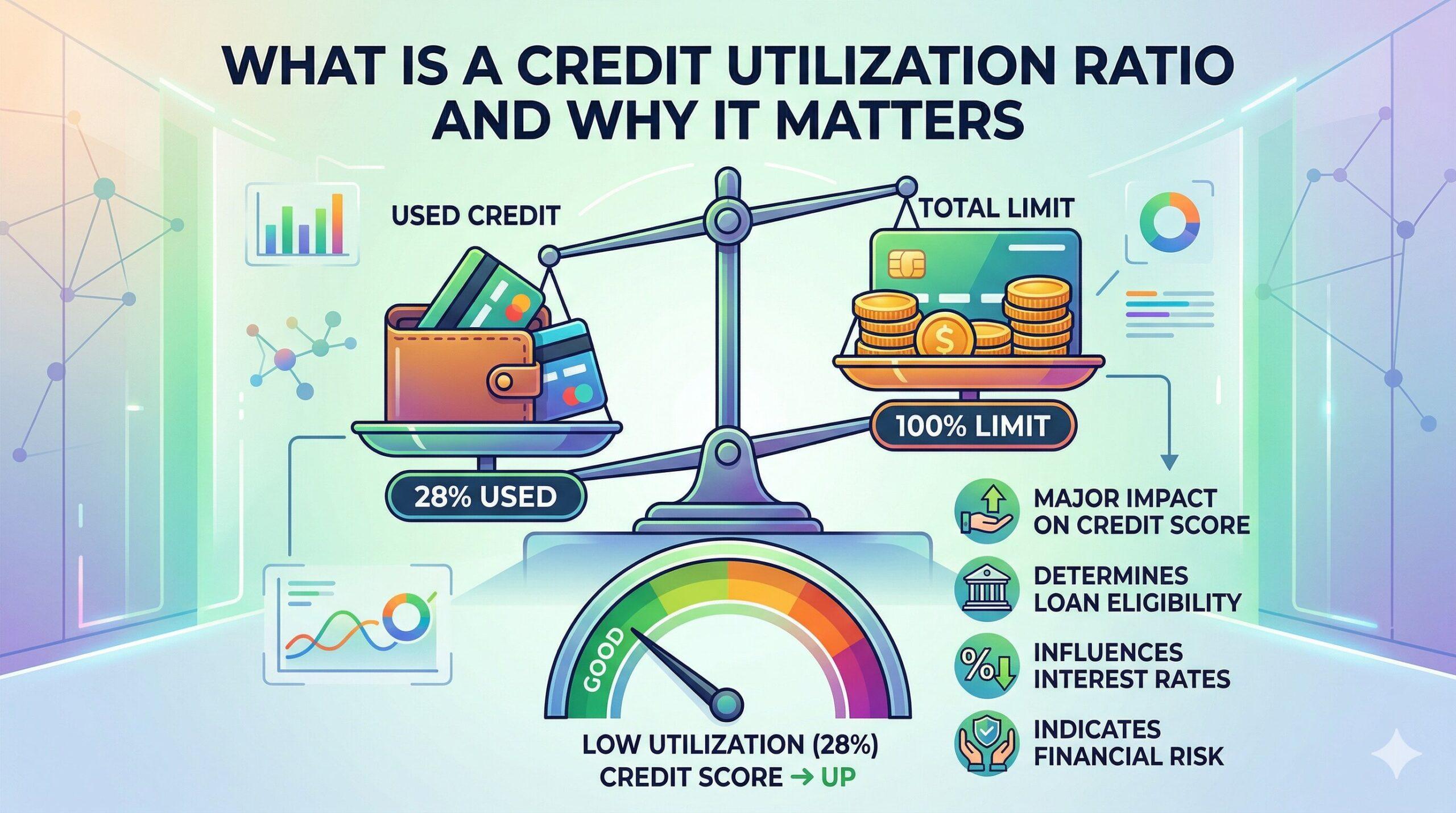

The Impact of Maxed Out Limits and Denied Applications

Your credit utilization ratio is one of the most important factors in your credit score, and hitting your limits is a loud siren that a crisis is imminent. If most of your credit cards are at ninety percent or more of their available limit, your score will begin to drop rapidly even if you have never missed a single payment. This “maxed out” status removes your safety net; if an emergency like a car repair or a medical bill occurs, you no longer have the available credit to handle it. Many people at this stage attempt to open a new credit card just to have a fresh line of available funds, only to find that they are denied due to “excessive obligations” or “high utilization.” Being denied credit when you feel you need it most is a definitive sign that the financial system now views you as a high-risk borrower.

You might also notice that your existing lenders are starting to take “adverse action” against you, such as lowering your credit limits or increasing your interest rates without a specific request. Lenders use automated systems to monitor your overall behavior across all your accounts. If they see you taking out a payday loan or if your score drops because of high balances on other cards, they may reduce your limit to protect themselves from potential loss. This creates a downward spiral where your utilization looks even worse because your available limit has shrunk, further damaging your score. If you find yourself looking into high-interest personal loans or “no credit check” lenders just to keep your head above water, you are at the final edge of a credit collapse. These types of loans often have predatory terms that make it nearly impossible to ever pay back the original amount borrowed.

Long Term Consequences and the Path Toward Recovery

The psychological toll of a credit crisis is often just as damaging as the financial impact. If you find that you are arguing with your spouse more frequently about money or if the sound of your phone ringing causes a spike in anxiety, your financial health is affecting your quality of life. You may also notice a decline in your work performance because you are spending your office hours trying to negotiate with creditors or moving money between accounts. Ignoring these signs does not make the debt disappear; it only allows the interest to grow and the legal options of your creditors to expand. Eventually, unaddressed credit crises lead to wage garnishments, bank levies, or the loss of assets through repossession or foreclosure.

The good news is that recognizing these ten signs early gives you the power to take a different path. The first step in recovery is a total “spending freeze” on all non-essential items to stop the bleeding of new debt. You must then create a rigorous, honest budget that lists every single dollar of income and every cent of debt. Seeking help from a reputable, nonprofit credit counseling agency can provide you with a structured Debt Management Plan (DMP) that often lowers interest rates and stops late fees. While it may take several years of disciplined effort to rebuild what was lost, starting today by acknowledging the crisis is the only way to ensure your future financial freedom. Do not wait until your credit report is beyond repair; take action the moment you see the first sign of trouble.

Leave a Reply