Budgeting with a steady paycheck is a challenge on its own. Budgeting when your income goes up and down every single month is an entirely different kind of problem. Freelancers, gig workers, seasonal employees, and commission-based workers all live with this reality every day. This guide gives you a practical system that works even when you have no idea what next month will bring.

Start With Your Baseline Income

Your baseline is the lowest amount you can realistically expect to earn in any given month based on your history. Look back at your income over the last 12 months and identify the three worst-earning months in that period. Take the average of those three months and use that number as your monthly planning baseline. This gives you a reliable floor to build your entire budget around without guessing.

Building your budget around your worst months rather than your average or best months keeps you out of financial trouble. When you earn more than the baseline, that extra money flows toward savings, debt paydown, or discretionary spending in that order. When income falls below the baseline, you already have your core needs covered and nothing critical gets missed.

Separate Your Needs From Your Wants

Fixed essential expenses are your highest priority in every month regardless of what you earned. These are recurring bills that must be paid whether your income was high or low this cycle. List every essential recurring expense and add them up to get your non-negotiable monthly floor. Nothing discretionary gets funded until this floor is fully covered each month.

These are the categories that count as essential expenses:

- Rent or mortgage payments

- Utilities including electricity, gas, and water

- Groceries and basic household supplies

- Health insurance premiums and medications

- Minimum debt payments on all loans and credit cards

- Transportation costs required to get to and from work

Everything beyond these six categories is secondary in any given month. Entertainment, dining out, subscriptions, and personal spending get funded only after every essential is paid in full.

Use a Tiered Spending System

A tiered spending system helps you make consistent decisions about where money goes when income varies month to month. Each tier gets funded in order from highest to lowest priority, and no lower tier gets money until the one above it is fully covered.

- Fund Tier 1 first by covering all essential expenses listed in the section above.

- Move to Tier 2 by contributing to your emergency savings account until you hit your monthly goal.

- Activate Tier 3 by paying extra on any non-essential debt beyond the required minimum payment.

- Spend Tier 4 on lifestyle items like dining out, streaming services, and personal care products.

- Direct any remaining income to long-term savings or investments once all four tiers are fully funded.

In a low-income month, you may only get through Tier 1 and part of Tier 2 before money runs out. That is exactly what the system is built for and it is not a failure.

Build an Income Buffer Account

An income buffer is a dedicated savings account designed to smooth out the peaks and valleys of variable income over time. Deposit all incoming money into this account first before spending anything. Then pay yourself a fixed monthly salary based on your baseline number regardless of what actually came in. This creates the psychological experience of a steady paycheck even when your real income fluctuates widely.

Start the buffer with one month of essential expenses as your initial target. Over time, build it up to cover two to three months of baseline needs. The buffer makes your monthly budget far more predictable and dramatically reduces financial stress during slow periods. Use an account at a completely separate bank to create enough friction that you do not dip into it casually.

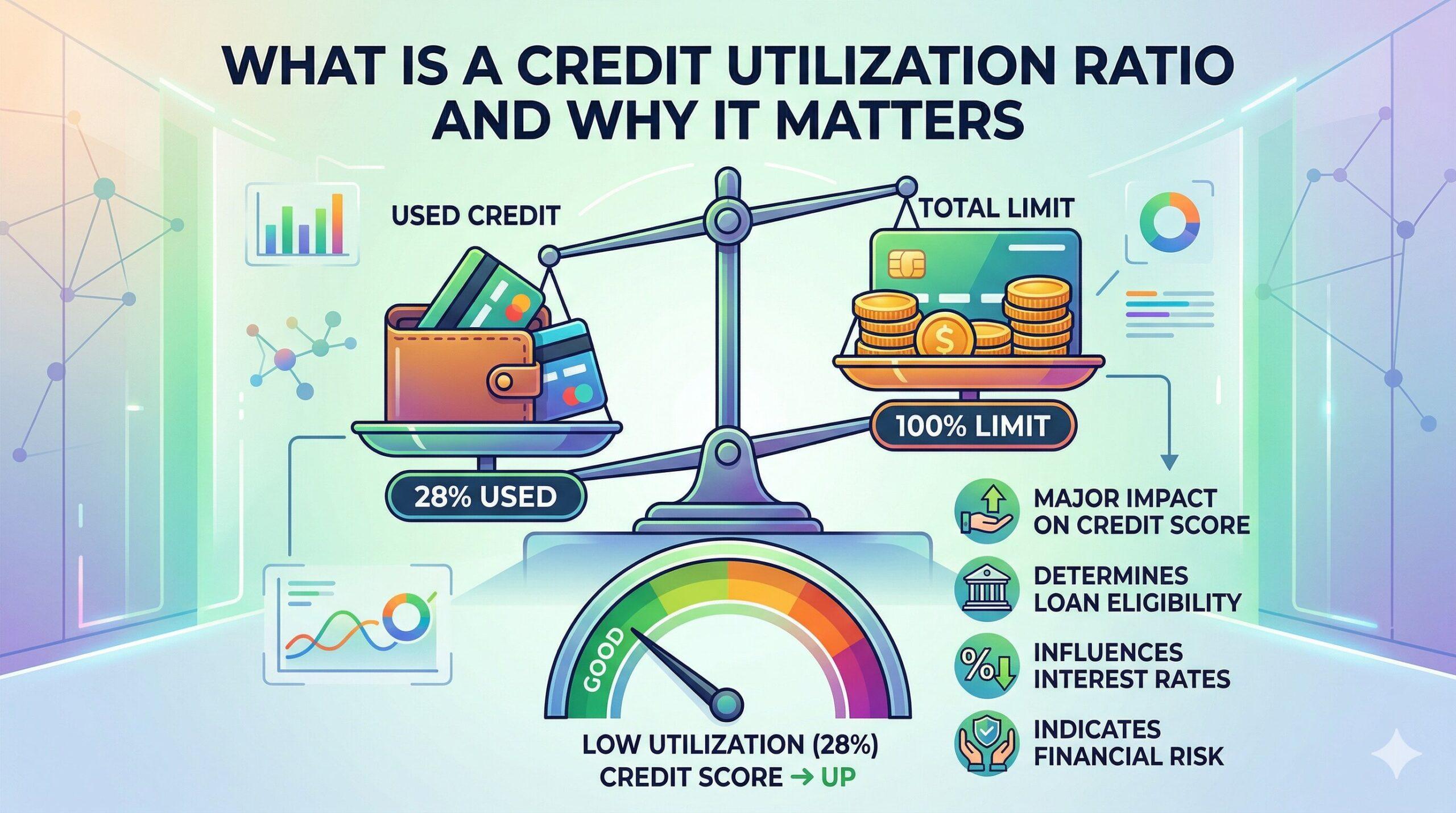

Track Your Credit During Low Months

Variable income months often push people toward credit cards as a bridge to cover gaps in cash flow. Watching your card balances closely during low months helps you avoid letting your credit utilization impact climb too high. A quick check before statement close each month costs you nothing and protects your score even during financially lean periods.

An emergency savings account is what makes the entire tiered system work reliably over the long term. Without savings to fall back on during a bad month, the whole budget structure collapses under the first unexpected expense. With even a modest cushion in place, you stay in control no matter what any given month decides to throw at you.

Variable income is not a budget problem. It is simply a budget design problem that requires a different approach than a traditional fixed-income plan.

Leave a Reply